NPS in India: How It Works, Real Returns, Withdrawal Rules and Smart Allocation Strategy

Super Policy Team •May 8, 2026 | 4 min read • 102 views

Super Policy Team •May 8, 2026 | 4 min read • 102 views

The National Pension System (NPS) is India’s market-linked retirement framework regulated by PFRDA. It offers very low costs, equity participation, and unique tax advantages, but trades these benefits for restricted liquidity and mandatory annuity exposure.

This guide is written for:

Retail investors building disciplined retirement savings

High-income salaried professionals optimising taxes

Self-employed professionals evaluating NPS alongside mutual funds

NPS is a defined-contribution pension system. Your retirement corpus depends entirely on:

Total contributions

Asset allocation

Market performance over time

There are no guaranteed returns. Unlike EPF or PPF, NPS invests in equity and debt markets.

Open an NPS account → receive PRAN (Permanent Retirement Account Number)

Select investment choice (Active or Auto)

Contributions are invested via PFRDA-approved fund managers

Corpus compounds until exit (normally age 60)

Partial lump sum + mandatory annuity at retirement

Key Takeaway

NPS is a long-duration, rules-driven product. Its strength lies in disciplined compounding, not flexibility.

Tier I Account Overview

Feature Details Purpose Retirement savings Withdrawals Restricted Tax benefits Yes Lock-in Till age 60

Tier II Account Overview

Feature Details Purpose Flexible investing Withdrawals Anytime Tax benefits No Lock-in None

NPS Asset Allocation Buckets

Asset Class What It Invests In Risk Level Equity (E) Listed Indian equities High Corporate Debt (C) Corporate bonds Medium Government Securities (G) Central & State bonds Low Alternative (A) REITs / InvITs (limited) Medium

Investor decides asset allocation

Equity capped at 75% till age 50, then gradually reduced

Suitable for informed investors

Allocation automatically adjusts with age

Three variants: Conservative, Moderate, Aggressive

Suitable for hands-off investors

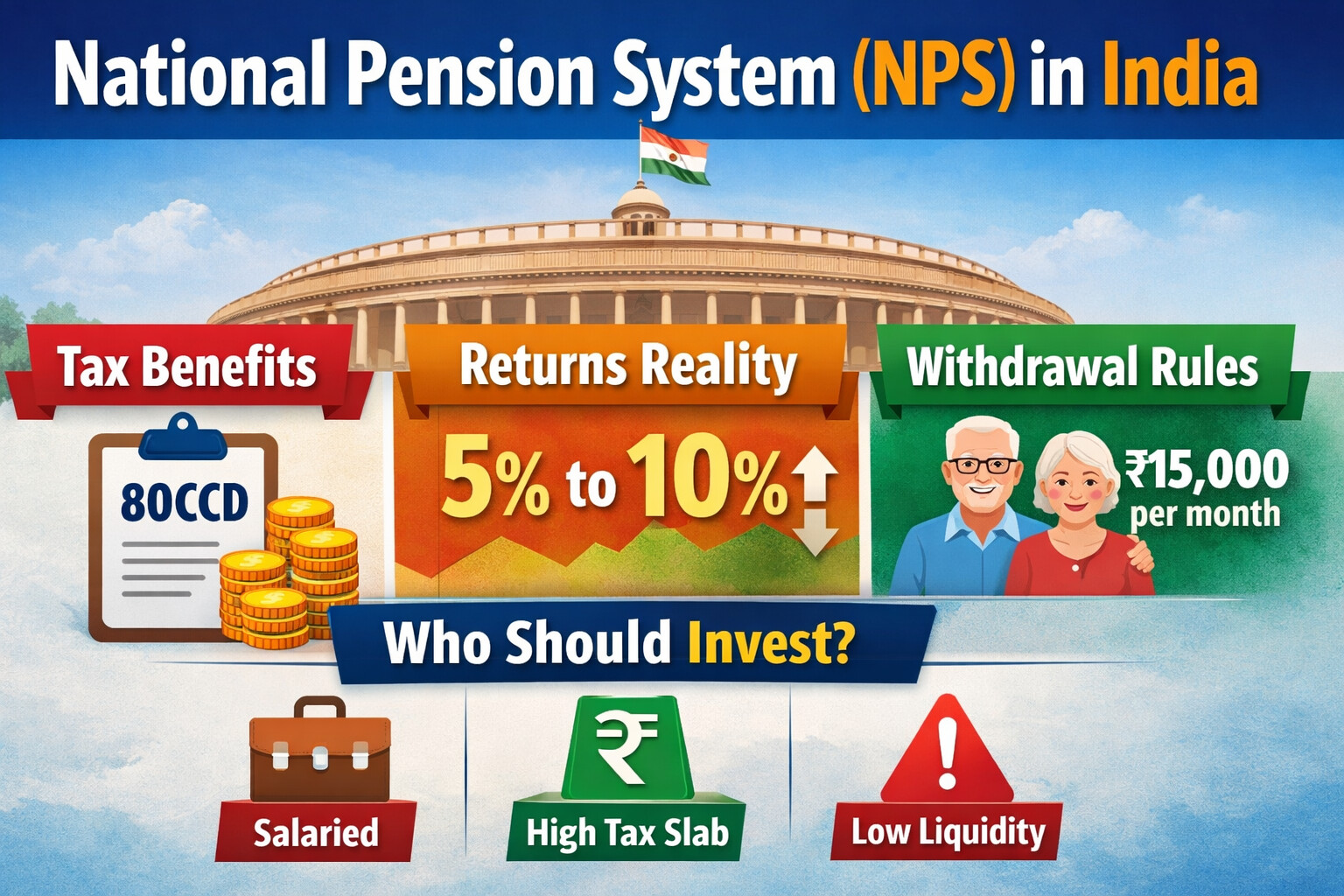

Historical long-term ranges (indicative, not guaranteed):

| Asset Class | Long-Term CAGR Range |

|---|---|

| Equity | 10–12% |

| Corporate Debt | 8–9% |

| Government Securities | 7–8% |

Returns vary by market cycles and fund manager performance.

NPS Tax Benefit Structure

Section Deduction Limit Eligible Investors 80CCD(1) Up to ₹1.5 lakh All individuals 80CCD(1B) Additional ₹50,000 All individuals 80CCD(2) 10%–14% of salary Salaried (via employer)

Important: Employer contribution under 80CCD(2) does not fall under the ₹1.5 lakh limit.

Key Takeaway

For high-income salaried investors, employer NPS contributions are one of the most powerful tax-saving tools available today.

NPS Exit at Retirement

Component Treatment Lump sum Up to 60% – Tax-free Annuity Minimum 40% – Mandatory

NPS Early Exit Rules

Component Treatment Lump sum Up to 20% Annuity Minimum 80%

Liquidity is the biggest limitation of NPS.

Key Takeaway

NPS rewards patience. If liquidity is a priority, it should not be your primary investment vehicle.

| Aspect | Details |

|---|---|

| Typical returns | 5–7% |

| Taxation | Fully taxable as income |

| Inflation protection | None |

Annuity choice materially impacts retirement income quality.

| Cost Component | Typical Level |

|---|---|

| Fund management fee | ~0.09% |

| CRA & admin charges | Very low |

NPS is among the cheapest long-term investment products in India.

Product Comparison Snapshot

Parameter NPS Mutual Funds EPF Returns Market-linked Market-linked Largely fixed Liquidity Low High Medium Tax at exit Partial LTCG applies Mostly tax-free Cost Very low Medium Low

High-income salaried individuals

Investors in 30% tax bracket

Those with EPF already maximised

Investors needing liquidity

Those seeking full control at retirement

Maximise employer contribution under 80CCD(2)

Prefer Active Choice with higher equity early on

Use NPS mainly for 80CCD(1B) tax benefit

Keep mutual funds as primary wealth engine

Policy and regulatory changes

Mandatory annuity exposure

Limited flexibility compared to mutual funds

Use NPS as a tax-optimised retirement layer, not a standalone wealth creator.

The most effective strategy combines NPS + EPF + equity mutual funds.

Key Takeaway

NPS works best as a supporting pillar in a diversified financial plan—not as the core engine of wealth creation.

This content is for educational purposes only and should not be considered investment advice. Tax laws and regulations may change. Consult a qualified financial advisor before investing.

Get the latest articles delivered to your inbox